Expansion revenue isn't a relationship outcome. It's a system connecting product usage signals, pricing tiers, and CS intervention timing — and the gap between where your net revenue retention sits today and where it needs to be is almost never a people problem.

Most SaaS companies have already tried to fix their NRR. They added expansion to their CS team's quarterly goals, ran a QBR refresh, invested in CSAT, and watched their NRR move two points — if they were lucky.

The problem wasn't effort. It was architecture. Expansion revenue doesn't improve because your CS team cares more. It improves because someone designed the triggers, the pricing tiers, and the intervention timing that make expansion the customer's natural next step.

A VP of CS carrying an NRR target without an expansion system is carrying a goal without a mechanism. At a Series B–D SaaS company, that gap compounds every quarter: the company is paying full CAC to replace revenue the installed base would generate at a fraction of the cost.

Benchmarkit's 2025 SaaS Performance Metrics report confirms the arithmetic — the median New CAC Ratio reached $2.00 in 2024, meaning companies spend two dollars in sales and marketing to acquire every dollar of new-logo ARR. The Expansion CAC Ratio, by contrast, sits at $1.00 at the median. The case for investing in existing customers is structurally superior.

Three forces have made this unavoidable in 2026. CAC has reached structural highs with no near-term relief. Investors now weigh NRR heavily in Series C and D underwriting — McKinsey's analysis of more than 100 B2B SaaS companies found that top-quartile NRR players sustain a median enterprise-value-to-revenue multiple of 24x, compared to 5x for bottom-quartile peers.

And Metronome and Greyhound Capital's January 2025 State of Usage-Based Pricing survey of 100 SaaS companies found that 85% have already adopted or are testing usage-based pricing — making programmatic expansion triggered by product behavior technically feasible at scale for the first time.

Companies stuck at 101–105% NRR have the product usage data, the customer relationships, and the pricing tiers that should be generating expansion. What they lack is the orchestration layer that connects those elements into a system.

As Crystal Kumpula, a revenue architect working with vertical B2B SaaS companies in the $10M–$50M ARR range, has observed:

The companies breaking through to 110–118% NRR aren't working harder on customer relationships — they're instrumenting expansion readiness as a measurable system capability.

This article introduces the Expansion Engine: a four-layer operational model connecting product usage signals, pricing architecture, CS intervention triggers, and expansion timing into a single auditable system.

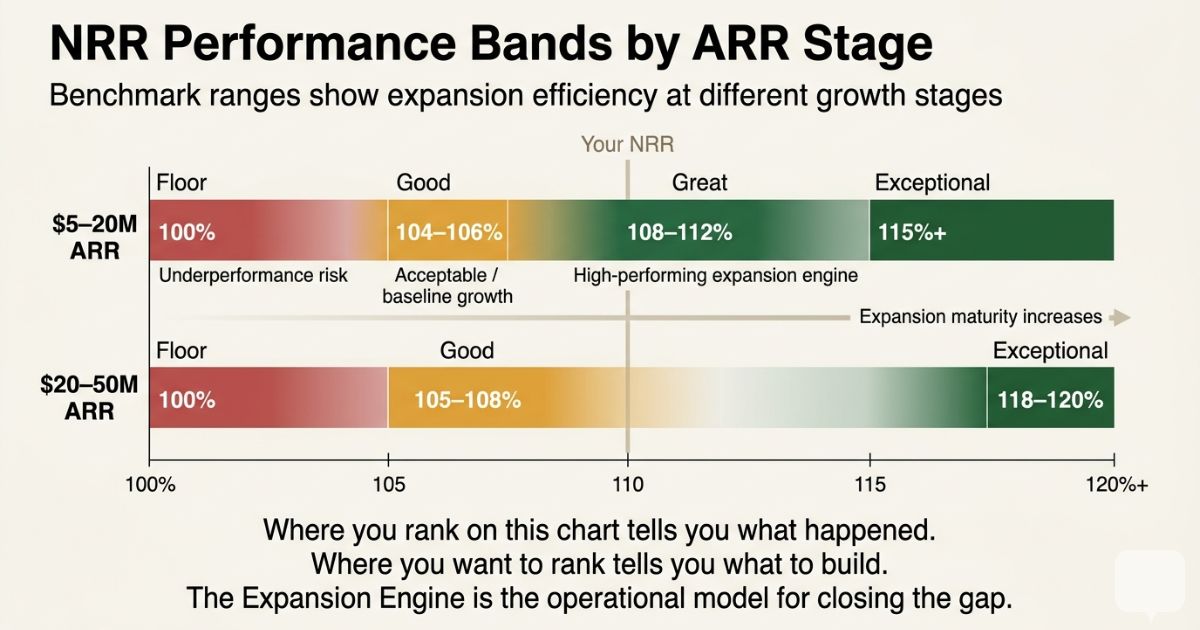

NRR Benchmarks by Stage — and Why Most Companies Read Them Wrong

NRR above 100% is not a CS performance score. It is evidence that expansion is happening faster than contraction — which tells you something happened, but nothing about whether it will happen again or whether you're capturing everything it could.

Net revenue retention measures the percentage of recurring revenue retained from existing customers over a period, including expansion, contraction, and churn, but excluding new-logo revenue. It is the single metric that tells investors whether your unit economics improve or degrade as you scale.

What Good Looks Like at Your ARR Stage

SaaS Capital's 2025 benchmarking data provides the calibration for the $3M–$20M ARR cohort — the median NRR for bootstrapped companies is 104%, with the 90th percentile at 118%.

At the $20M–$50M stage, the bars shift upward. High Alpha's 2025 SaaS Benchmarks Report found that top-quartile companies (above 106% NRR) generate an incremental $4M in ARR through expansion from a $20M base, while bottom-quartile companies (below 98%) lose $1M to churn — creating a $5M gap in new-logo requirement between the two cohorts.

Companies sitting at 101–105% at either stage aren't failing on retention. They're failing to capture the expansion the product economics already support.

The critical distinction is between NRR that happened to you and NRR you engineered.

Organic expansion — customers who upgraded because they hit a usage limit or self-discovered the premium tier — is real revenue, but it's a floor, not a system. It tells you expansion intent exists in your customer base. It tells you nothing about what percentage of that intent you're capturing, or how to make it predictable.

In one illustrative case shared by a B2B SaaS founder, NRR moved from 94% to 108% in twelve months. The underlying demand was already there — customers were using the product in ways that signaled expansion readiness.

The system to detect and act on those signals was not.

The gap between 94% and 108% wasn't a relationship gap. It was an instrumentation gap.

Why Your CS Team Can't Fix NRR — The Incentive Architecture Problem

The organizational design problem is worth being direct about: a CS team measured on CSAT and GRR cannot systematically improve expansion ARR — not because the people are wrong, but because the incentive architecture is.

What gets measured gets optimized.

A CS team measured on retention scores and ticket resolution will optimize for customer satisfaction and churn prevention. These are the right behaviors for GRR.

They are the wrong behaviors for expansion ARR — which requires identifying product usage signals, initiating conversations at value realization moments, and moving customers through pricing tiers at the highest-conversion window.

That's a different job, requiring different triggers, different data inputs, and different workflow logic.

Adding an expansion quota to a CSAT-measured CS team doesn't change this. It changes a number in the OKR without changing the system the team operates inside.

The quota lands as an additional target on a team already optimized for a different outcome — and the result is the one most CS leaders reading this have already experienced: the expansion number gets attention at QBR time and stays flat the rest of the quarter.

Anand Vatsya, who leads growth at Storylane, documented what actually works.

Storylane was generating approximately 20% of ARR from expansion organically, without a deliberate system. When they tried adding expansion as a motion on top of existing outbound workflows, results were marginal.

When they built entirely separate expansion infrastructure — dedicated signal tracking, a distinct research process, separate messaging frameworks, dedicated capacity — expansion contribution roughly doubled to over 40% of new monthly ARR within three months.

As Vatsya described it:

They stopped trying to fit expansion into the existing outbound motion and instead built an entirely new one from scratch.

Benchmarkit's 2025 data confirms the broader pattern: existing customers now generate 40% of total new ARR across private B2B SaaS, up from 25% in 2022 — but primarily among companies that have built the infrastructure to capture it.

The organizational design implication is explicit: expansion doesn't scale by adding quota. It scales by building the motion that quota is supposed to be measuring.

NRR is not a CS metric. It is a cross-functional system output. Owning NRR means owning the system.

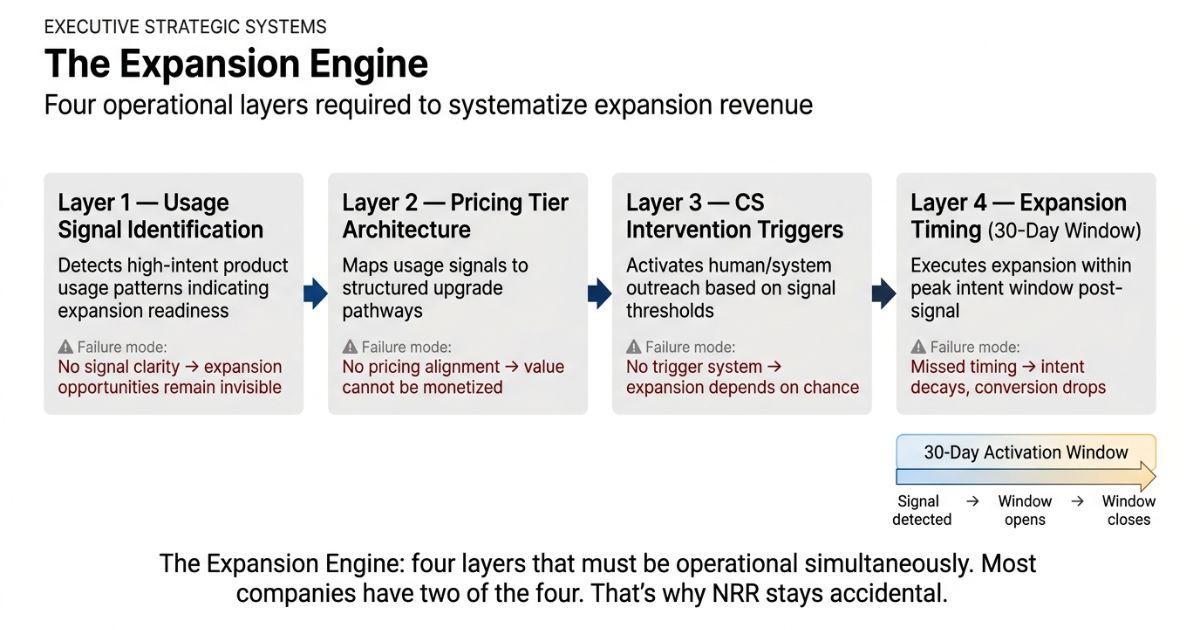

The Expansion Engine — Four Layers That Make Expansion Revenue Predictable

The Expansion Engine connects the four components that, when present and instrumented together, convert expansion from accidental to engineered.

Each layer can be assessed independently. All four must be operational for NRR to become predictable.

Layer 1 — Usage Signal Identification

Which product behaviors predict expansion readiness in your customer base?

The signals that reliably generate expansion intent are those tied to value realization milestones:

- Approaching a usage threshold that limits what the customer can do

- Reaching feature adoption depth that indicates the workflow is embedded

- Completing a pattern that predicts the next logical use case

A customer who logged in three times last month and a customer who hit 85% of their seat limit and completed the three most value-intensive workflows are not the same expansion opportunity.

The first may need re-engagement. The second is ready to expand — and the window to act is roughly 30 days before the moment passes.

Layer 2 — Pricing Tier Architecture

Expansion must be the customer's natural next step, not a sales conversation they have to agree to be pitched on.

If your pricing tiers don't create a self-evident upgrade path at the moment of maximum value realization, you're depending on human intervention to close a gap the product should close.

The B2B SaaS founder referenced above illustrates this precisely. After two years at 94% NRR with near-zero deliberate expansion, they added:

- A usage-based pricing component

- A one-click upgrade trigger at usage limits

- An add-on product

- Monthly-to-annual conversion incentives

Expansion went from negligible to 18% of new MRR within twelve months.

The one-click upgrade path alone drove the majority of the total gain — no additional headcount, no new CS workflow, just a pricing tier that made the next step obvious at the moment the customer needed it.

For companies not yet on usage-based models, Layer 2 still applies: the question is whether your pricing tiers create natural progression moments at value realization points, or whether expansion always requires a human to initiate it.

Rob Litterst, a pricing strategist who advises SaaS companies on expansion architecture, has identified why seat-based models are weakening as growth levers: as AI reduces the headcount that historically justified per-seat pricing, the expansion trigger model must shift to usage depth and workflow value.

Layer 3 — CS Intervention Triggers

The orchestration layer is where most expansion systems break down.

Product usage signals exist in analytics dashboards. Pricing tiers exist in the billing system. But the behavioral signal that should automatically populate a CS rep's workflow with a specific action and a specific message doesn't exist in most organizations — the signal and the action are disconnected.

Crystal Kumpula describes what a working system looks like: when behavioral signals automatically trigger CS workflows and appear in CRM expansion pipeline views, NRR becomes predictable rather than random.

The shift is from CS teams reviewing accounts on a calendar cadence to CS teams activating on system-generated signals.

This layer requires RevOps instrumentation:

- Product signals mapped to CRM triggers

- Expansion opportunities treated as a forecastable pipeline

- Defined stages and ownership

If your CRM has no expansion pipeline view, Layer 3 is not operational regardless of how strong your product analytics are.

Layer 4 — Expansion Timing

The highest-conversion expansion window is within 30 days of an activation milestone — not at renewal.

Most CS teams are calendared around contract dates because that's when upsells have traditionally been discussed.

But the customer's propensity to expand is highest when they're actively experiencing the value the product delivers, not when a contract renewal surfaces the pricing question in a context that feels like a sales pitch.

SaaS Capital's 2025 research found that increasing NRR from the 90–100% range to the 100–110% range is associated with a five percentage point improvement in company growth rate — and that improvement compounds each quarter as expansion ARR accumulates before renewal cycles even begin.

What the NRR Benchmarks Tell You When You Read Them as a Design Brief

Benchmarks are most useful not as validation of where you are, but as targets for what the system must produce.

McKinsey's analysis of more than 100 B2B SaaS companies found that top-quartile NRR players sustain a median enterprise-value-to-revenue multiple of 24x compared to 5x for bottom-quartile peers, from Q1 2019 through Q4 2024.

Windsor Drake's 2025 SaaS Valuation analysis confirms the same pattern in public market data: companies with NRR above 120% trade at approximately 8x revenue, while those in the 100–110% range trade at around 6x — a nonlinear premium where improvements above 110% tend to produce disproportionate multiple expansion.

At Series C and D, NRR has become a primary underwriting variable because it tells investors whether the business's unit economics improve or degrade as it scales.

The expansion ARR contribution data makes the structural case concrete.

Benchmarkit's 2025 report — drawing on data from 1,600+ private B2B SaaS companies — found that existing customers now generate 40% of total new ARR, up from 25% in 2022.

High Alpha corroborates this directionally: companies above $50M ARR now generate roughly 60% of new ARR from existing customers.

The direction is consistent across sources. Leading SaaS companies are generating a growing majority of new ARR from expansion rather than purely from new-logo acquisition — a structural shift in how growth is funded that makes a systematic expansion motion non-optional.

Companies stuck at 101–105% NRR aren't three points from good. They're an Expansion Engine build away from it.

High Alpha's 2025 benchmarks found that companies pairing high NRR with low CAC payback are associated with nearly double the growth rates and Rule of 40 scores compared to peers with weaker retention or longer paybacks.

The expansion motion doesn't compete with acquisition — it makes acquisition more efficient by increasing the value of every logo already acquired.

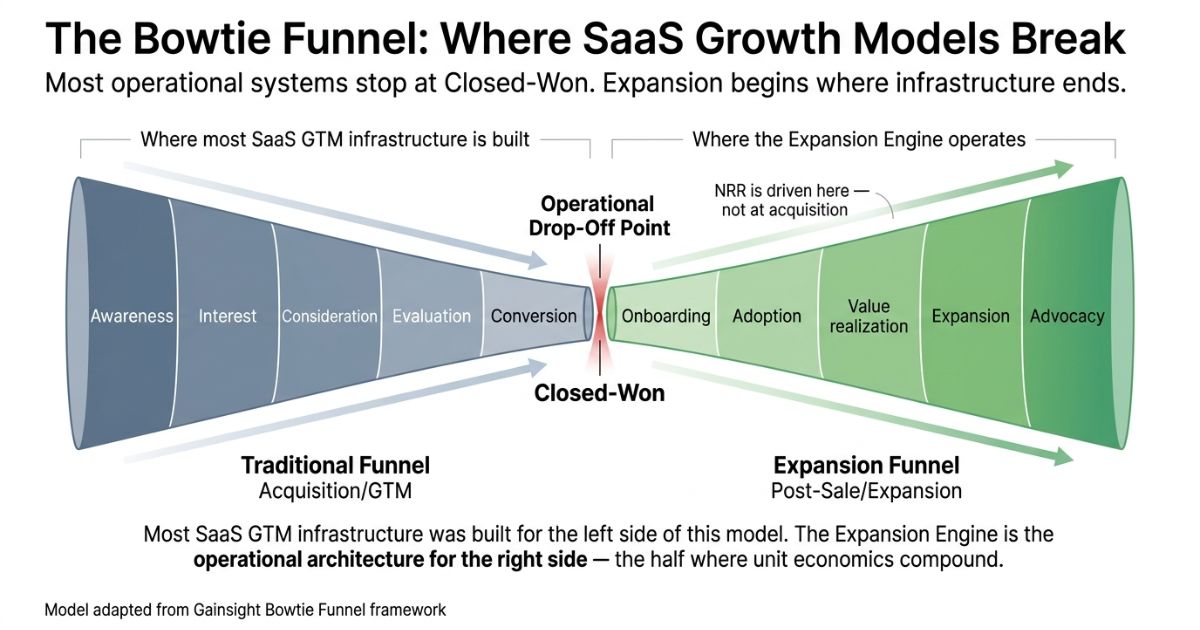

The Bowtie Funnel — developed by Gainsight and widely deployed in CS strategy — shows where most SaaS growth models terminate prematurely.

The standard acquisition funnel ends at conversion. The Bowtie continues through adoption, expansion, and advocacy.

Most SaaS companies have built the left side of the funnel in detail and left the right side without instrumentation, ownership, or forecast discipline.

The Expansion Engine is the operational architecture for the right side.

Three Audit Questions to Test Whether Your CS Motion Is Built for Expansion

These three questions can be answered in a working session with your CS and RevOps leads before the next board meeting.

- Do your usage signals automatically trigger CS workflows, or does expansion depend on a CS rep deciding which accounts to prioritize?

If expansion intent lives in a product analytics dashboard that CS reviews monthly on a calendar cadence, Layer 3 is not operational.

Expansion that depends on a human remembering to check an account is a random variable, not a system.

-

Does your pricing architecture create a self-serve upgrade path at your highest-value feature threshold, or does every expansion conversation require a human to initiate it?

If every upsell requires a CS-initiated discovery conversation, you're adding friction to the highest-conversion expansion window.

One self-serve upgrade trigger at the usage limit closest to your highest-value feature costs less to build than one enterprise sales hire — and produces expansion that doesn't require the sales cycle.

The founder case above — NRR moving from 94% to 108% — was driven primarily by this single architectural change.

-

Is expansion ARR a forecastable pipeline in your CRM — with its own stages, ownership, and close-rate data — or is it a line item in a quarterly NRR report?

If expansion doesn't have a pipeline view, it doesn't have a forecast.

If it doesn't have a forecast, it doesn't have an owner.

And if it doesn't have an owner, the NRR target the board set is a number with no mechanism behind it.

If the answer to any of these is "no" or "not sure," the Expansion Engine is not operational — and NRR improvement will remain accidental.

Build the System, Not the Relationship — How SaaS Retention Gets Engineered in 2026

The three sections of this argument connect in sequence.

CS teams can't optimize for expansion ARR when their incentive architecture measures something else — not because the people are wrong, but because the system they operate inside is optimized for a different output.

The Expansion Engine addresses the system, not the people: four layers that, when instrumented together, convert product usage data into triggered CS actions at the highest-conversion window, through pricing tiers that make expansion the customer's natural next step.

The audit questions make the gap visible before the next board conversation surfaces in the NRR report.

The sequencing decision is the immediate one.

- If product telemetry isn't instrumented, start with Layer 1 — no other layer is operable without it.

- If the telemetry exists but doesn't trigger CS workflows, Layer 3 is the constraint.

- If CS has the signals but converts at low rates because every upgrade requires a manual conversation, Layer 2 is where the friction lives.

The companies generating 110%+ NRR in 2026 didn't hire better CS teams. They built a better system — and the NRR is the system's output, not its cause.

Frequently Asked Questions

What is a good net revenue retention benchmark for B2B SaaS?

For companies at $3M–$20M ARR, SaaS Capital's 2025 data puts median NRR at 104%, with 90th-percentile performers at 118%.

At the $20M–$50M stage, top-quartile NRR exceeds 106%.

Companies consistently above 110% NRR are considered best-in-class and command significantly higher revenue multiples at Series C and beyond.

How does NRR differ from GRR in B2B SaaS?

Gross revenue retention (GRR) measures retained revenue after churn and contraction, capped at 100%.

Net revenue retention adds expansion revenue, allowing it to exceed 100%.

GRR tells you how well you protect existing revenue; NRR tells you whether existing customers are growing — making NRR the more relevant metric for evaluating expansion system performance.

Why can't CS teams improve NRR by focusing on customer satisfaction?

CSAT and ticket resolution optimize for churn prevention — the right behaviors for GRR.

Improving NRR above 105% requires a different motion:

- Product usage signal detection

- Pricing tier architecture that creates self-serve upgrade paths

- RevOps-instrumented triggers that route expansion opportunities into a forecastable CRM pipeline

These are system-design problems, not relationship problems.

What percentage of ARR should come from expansion revenue?

Benchmarkit's 2025 data shows that among companies with built expansion infrastructure, existing customers now generate 40% of total new ARR — up from 25% in 2022.

Companies above $50M ARR with mature expansion motions generate roughly 60% of new ARR from existing customers.

When is the best time in the customer lifecycle to trigger an expansion conversation?

Within 30 days of an activation milestone — not at renewal.

Customer propensity to expand tends to be highest when they're actively experiencing product value.

Renewal-timed upsells introduce pricing friction at a moment the customer is least engaged with usage benefits.